Blogs

Banks and NBFCs are sitting on the same problem they have had for decades. Too many documents, too many handoffs, and not enough time. AI agents are finally changing the math.

The Approval Problem Nobody Talks About Loudly

Walk into any mid-size NBFC or private bank and ask a senior credit officer how long a typical SME loan approval takes. If they are being honest, they will say somewhere between five and fifteen business days. Then ask them how much of that time is spent on actual risk assessment. Most will pause before admitting: maybe a day, if that.

The rest is waiting. Waiting for documents to arrive. Waiting for a compliance check to complete. Waiting for the underwriting queue to clear. Waiting for someone in legal to review the same clause they have reviewed four hundred times before.

This is not a people problem. The teams involved are often sharp and experienced. It is an architecture problem. One built before AI agents existed.

What Is an AI Agent, Actually?

There is a lot of noise around AI agents right now, and a lot of it is vague. So let us be specific.

An AI agent is not just a chatbot or an automation script. It is a system that can observe context, make decisions, take actions, and hand off to other agents or humans based on what it finds. It can work across multiple systems simultaneously, not sequentially. It can read unstructured data like scanned documents or free-text financial notes, not just structured database fields.

In a credit workflow, that means an agent can pull a borrower's bank statements, cross-reference them with bureau data, flag income inconsistencies, check against internal policy rules, and draft a preliminary credit memo; all before a human underwriter has opened their inbox.

That is not an exaggeration. It is where several leading institutions already are.

Where the Credit Lifecycle Actually Loses Time

Before looking at where AI agents plug in, it helps to map where the delays actually live. Most credit journeys have five or six points where things slow down:

Each of these steps, individually, is manageable. Together, they create a process that moves at a pace borrowers increasingly find unacceptable, especially when fintech lenders are offering decisions in under an hour.

How AI Agents Rewire Each Stage

Document Intake and Triage

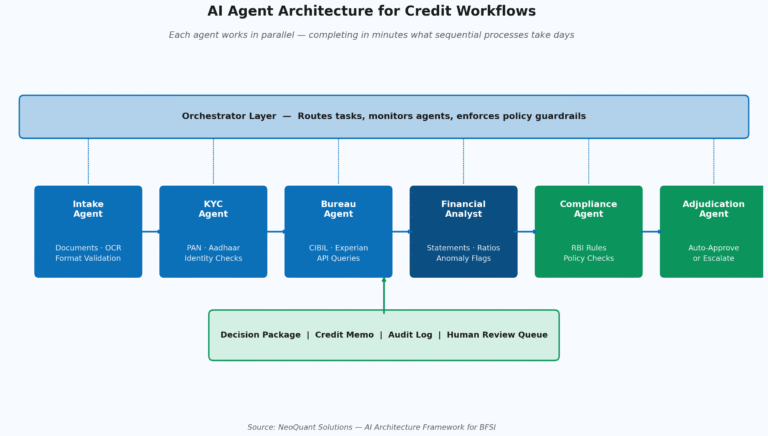

An intake agent can receive documents in any format: PDF, image, email attachment, and immediately classify, extract, and validate them. If something is missing or unreadable, the agent sends a targeted follow-up request automatically. What used to require a back-and-forth over two or three days happens in minutes.

Identity and Bureau Verification

Verification agents connect directly to CIBIL, Experian, and internal KYC systems via API. They do not wait for a human to log in, navigate a portal, and copy data across screens. They run in parallel, which means multiple checks complete simultaneously rather than sequentially.

Financial Statement Analysis

This is where AI agents add the most visible value. A financial analysis agent can ingest three years of bank statements, compute key ratios, identify irregular transactions, cross-reference declared income with actual inflows, and flag patterns that suggest elevated risk. It can do this for thirty applications at once, with consistent logic applied to every single one.

McKinsey research indicates banks using LLMs for borrower data extraction and statement analysis report time savings of 30 to 50 percent on credit memo preparation alone.

Policy and Compliance Checks

Compliance agents monitor evolving regulatory requirements in real time. Instead of underwriters manually checking whether an application meets the latest RBI guidelines or internal credit policy updates, an agent does it automatically — and logs every check for audit purposes.

Adjudication and Escalation

Not every loan gets auto-approved, nor should it. The final adjudication agent packages the complete decision context: risk score, supporting data, exception flags, and a plain-language rationale. It either auto-approves within defined thresholds, auto-declines with documented reasons, or escalates to a human underwriter with everything they need to make a fast, informed decision.

The human is still in the loop. They are just working on the thirty percent of cases that genuinely need their judgment, not the seventy percent that do not.

What This Looks Like in Numbers

The shifts showing up across implementations are significant enough to have changed how institutions think about headcount and capacity:

Consumer lending studies show loan processing times drop by 50 to 70 percent when AI-enabled workflows coordinate intake, verification, and underwriting simultaneously.

Multiagentic AI systems have been shown to deliver 40 to 80 percent productivity uplift per use case, with greater consistency across outputs - McKinsey Risk and Resilience Practice, 2025.

For an NBFC processing a few thousand loan applications a month, that kind of compression does not just improve efficiency. It changes what is possible. You can serve more borrowers with the same team, reduce NPA risk through more consistent underwriting, and compete on turnaround time, which is increasingly how borrowers choose lenders.

The Implementation Trap Most Institutions Fall Into

Here is where most AI agent conversations go wrong. Institutions focus on the agent layer — the models, the interfaces, the orchestration logic, without first fixing what the agents will be working with.

An agent that pulls from fragmented, unvalidated data sources will produce fragmented, unvalidated outputs. The quality of the intelligence is downstream of the quality of the data infrastructure. If bureau APIs are unstable, if bank statement data is inconsistently formatted, if internal policy documents are scattered across SharePoint folders, the agent cannot do much with any of it.

The institutions that get this right treat data readiness as the prerequisite, not the afterthought. They build clean, governed pipelines before they build the agent layer on top.

That sequencing matters. And it is often where external expertise: in data engineering, system integration, and AI architecture makes the difference between a pilot that works and a deployment that scales.

The Real Question for Your Institution

If you are a CRO or CTO at a bank or NBFC reading this, the question is not whether AI agents can compress your credit lifecycle. The evidence on that is clear enough. The question is whether your current data and systems infrastructure can support agents that are reliable, auditable, and regulatorily defensible.

Most institutions are closer than they think, but the path from where they are to where they need to be requires a clear architecture assessment, not just a tool selection exercise.

If you want to understand where your institution stands and what a phased AI implementation roadmap could look like, NeoQuant works with banks and NBFCs to build that foundation - from data pipelines through to production-grade AI deployment.

Start with a conversation

FREQUENTLY ASKED QUESTIONS

Can AI agents fully replace loan underwriters?

No, and the best implementations are not trying to. AI agents handle the repeatable, data-heavy parts of the credit process - document extraction, bureau checks, ratio computation, policy validation. Human underwriters step in for edge cases, relationship-sensitive decisions, and final sign-off on high-value loans. The practical outcome is that underwriters spend their time on the thirty percent of applications that genuinely need judgment, rather than the seventy percent that do not. That is a productivity shift, not a headcount elimination.

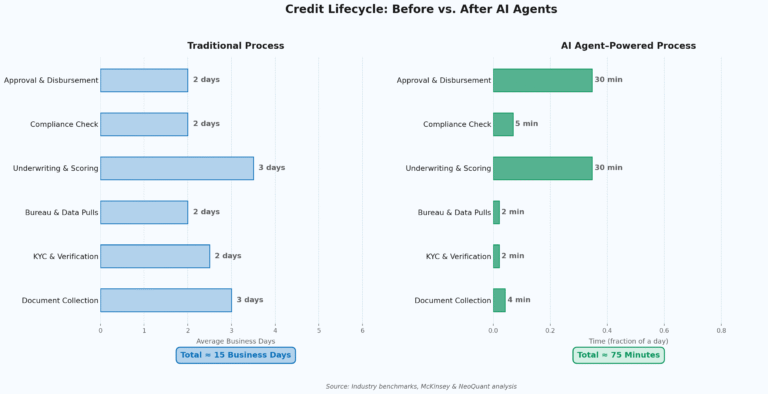

How long does AI-powered credit processing actually take?

For a standard retail or SME loan application where documents are complete, end-to-end AI processing - from document intake through to a decision recommendation - can run in under 75 minutes. Compare that to the five to fifteen business days most mid-size NBFCs and banks operate on today. The compression is most dramatic at the document triage and bureau verification stages, where what previously took two to three days of back-and-forth now happens in minutes via automated API calls.

Do AI agents work with existing core banking systems, or do you need to replace them?

You do not need to replace your core banking system. AI agents integrate with existing infrastructure through APIs and middleware layers; they sit on top of your current LOS, CRM, and bureau connections rather than replacing them. The more relevant question is whether your existing systems can expose the data AI agents need in a consistent, accessible format. That is a data engineering challenge, not a core banking replacement decision.

What are the regulatory and audit implications of using AI in credit decisions?

Any AI system used in credit decisioning needs to produce explainable, auditable outputs, meaning every decision must come with a documented rationale that compliance teams and regulators can review. Well-designed AI agent systems log every action, every data point used, and every rule applied. That audit trail is actually more complete than what a manual underwriting process typically produces. RBI guidelines on model risk management and algorithmic fairness apply, and any deployment should be assessed against them before going live.

Which types of loans benefit most from AI agent automation?

High-volume, standardised products see the fastest and clearest ROI - personal loans, consumer durables, vehicle loans, and SME working capital. These have defined eligibility criteria, predictable document sets, and enough volume to justify the integration investment. Bespoke corporate credit, project finance, and large-ticket structured loans still benefit from AI assistance at specific stages, but the end-to-end automation case is stronger for retail and MSME lending.

About NeoQuant Solutions

NeoQuant is an AI, Data Engineering, Cloud, and Application Development company with over twenty years of experience building enterprise-grade technology solutions for large financial institutions, banks, and NBFCs across India.